How much money will go into your pocket after your home is sold?

by Kalen Isas

How much money will go into your pocket after your home is sold?

It’s not what you make, it’s what you keep that matters. This holds especially true when it comes to the sale of your home.

The sales price you see at the top of the closing paperwork is rarely, if ever, the amount of money that ends up in your pocket as the seller.

There are often a variety of costs and fees associated with getting a home sold, so it’s important that you understand exactly what you’re going to walk away with before you put a sign in your front lawn to let the world know it’s for sale.

The smart thing to do is to consult with a great local agent and have them go over what industry experts call a net sheet.

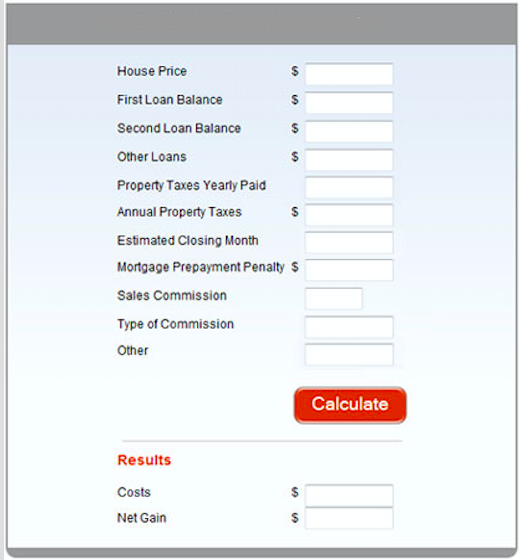

A net sheet is a financial worksheet that takes the sales price of a listing and then subtracts what the costs and fees are to get a home sold, giving you the net proceeds from the sale of the home.

The math is simple and when done correctly, it will give you an extremely clear picture of what you’ll walk away with when you sell your home.

Here’s a sample net sheet that a real estate agent would use with you prior to listing your home to make sure you knew what selling your home meant to you financially.

Let’s take a closer look at how much money will go into your pocket after your home is sold.

House price: This one speaks for itself. It’s not the price at which your home is first listed, it’s the price at which the home actually sells when all is said and done. There’s a strong possibility that it will be the same number, but it’s important that you understand the selling price of your home could be higher or lower when it finally sells.

First loan balance: This amount usually represents the original mortgage you took out on your home when you first bought your house. Ideally, it’s the main lien holder on your house.

Second loan balance: If you took out a second mortgage or home equity loan, this would qualify as a second loan balance.

Other loans: If you took out a third loan on your home or pledged it as collateral, it would show up here. Or, if there’s another loan you’d like to pay off with the mortgage, you would list it here.

Property taxes yearly paid/Annual property taxes: This one is a bit misleading. The reason is that your property tax allocation is going to be prorated based upon when you actually close your home. You’ll get credit for whatever you already paid or charged for the time you’ve lived in the home that you haven’t paid for yet. The company or attorney that closes the transaction when your home sells will do the research and reflect whatever the amount is that needs to go here.

Estimated closing month: You put that month here because you want to determine how the prorations for taxes, insurance and utilities would look based upon the month in which you would close on the sale of your home.

Mortgage prepayment penalty: If you got a loan that required you to stay in your home for a period of time before you sold it and then subsequently charges a payment if you do sell early, then you would enter that penalty amount here.

Sales commission: This is the line where you would enter the commission that your agent would earn from helping you sell your home.

Other: In this category, you would put any repairs you needed to make to get the home sold for top dollar, any points you’re paying for the buyer or any closing costs you’re covering for the buyer at closing.

Now, let’s put this into some real numbers for you:

House Price: $250,000

First Loan Balance: $125,000

Second Loan Balance: $18,000

Other Loans: $3,000

Annual Property Taxes: $2,500

Estimated Closing Month September

Mortgage Prepayment Penalty: $0

Sales Commission: $15,000

Other: $0____________

Net Proceeds: $86,500

In this instance, the seller would walk away with roughly $86,500. Again, prorations for taxes, insurance, utilities, etc. will alter that amount. The good news is that the seller would find out exactly what these numbers look like on the Truth In Lending Act (TILA) sheet provided to them at closing before they sign on the dotted line to transfer the home.

If you’re looking to sell, be sure you consult with a good real estate agent who can first price your home properly and second, identify all the fees and costs associated with getting your home sold so you’ll know roughly what you’ll walk away with at closing.

Recent Posts

- 10 questions you must ask an agent before you list your home

- How to beat other buyers to hot, new listings (Before they even know about them)

- When is the Best Season of the Year to Buy to get the Best Deal

- How much you should put down to purchase your new home?

- Why You Should Get a Home Warranty When You List Your Home